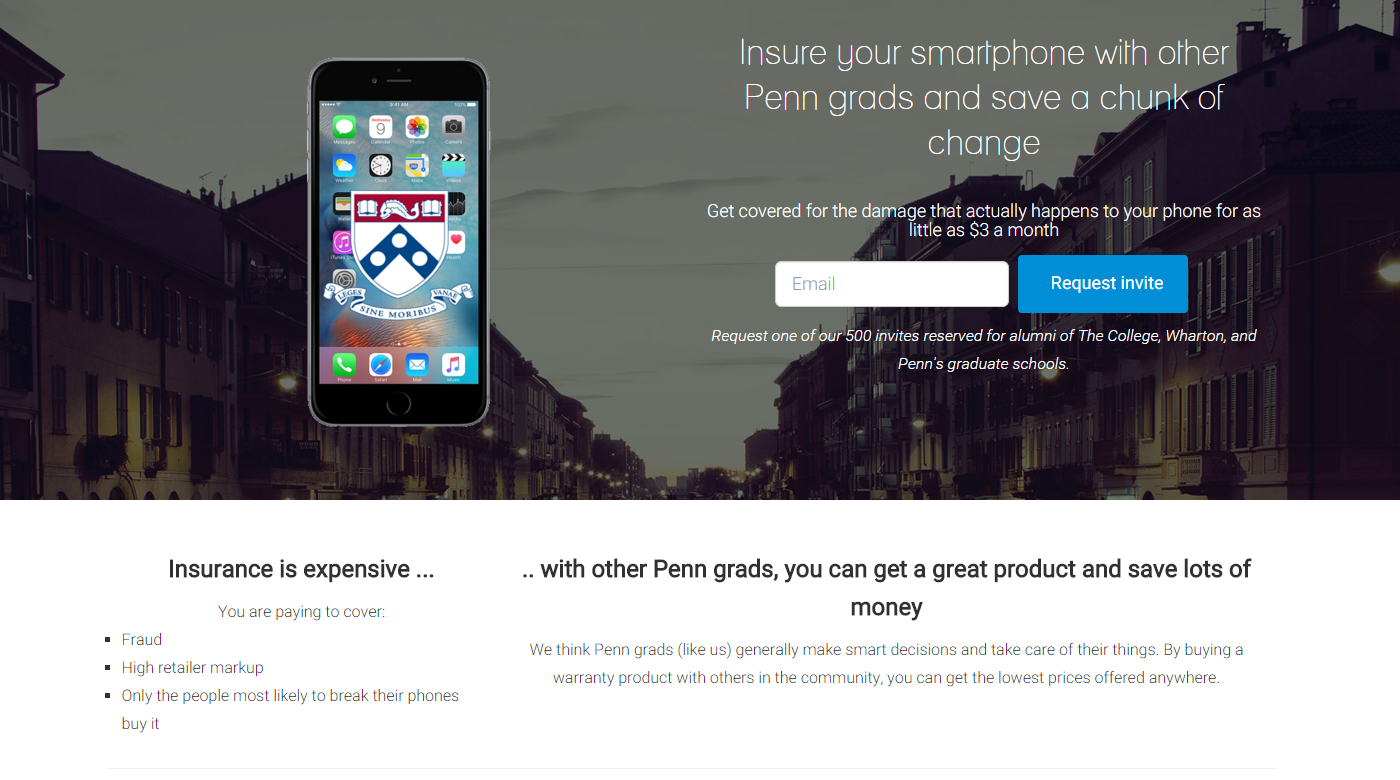

A friend directed my attention to a startup-y website selling “cheap smartphone [insurance] coverage” for “as little as $3 a month”. Right at the top of the Penn-branded subdomain (penn.getcovered.co) was an iPhone mockup showing the Penn shield:

Outside sponsors of University programs or activities often seek to use University names or insignia in promotional or advertising materials. While the University is pleased to recognize the contributions of sponsors, such recognition must not suggest University endorsement of the sponsor’s activities. Therefore, University names or insignia may not be used in connection with any outside entity’s name or logo without prior approval of the Secretary of the University. In general, the Secretary will approve uses which recognize or acknowledge the sponsor’s contribution to the University program or activity. Uses which, in the Secretary’s judgment, may suggest University endorsement or approval of the sponsor’s goods or services will not be permitted.

The big issue, of course, is the risk of confusion — by consumers, etc — who might think that the service is sponsored or endorsed by the university. There would be a pretty good prima facie case for trademark infringement, especially since the registrant behind the domain name appears to be a Stanford grad with no connection to Penn.

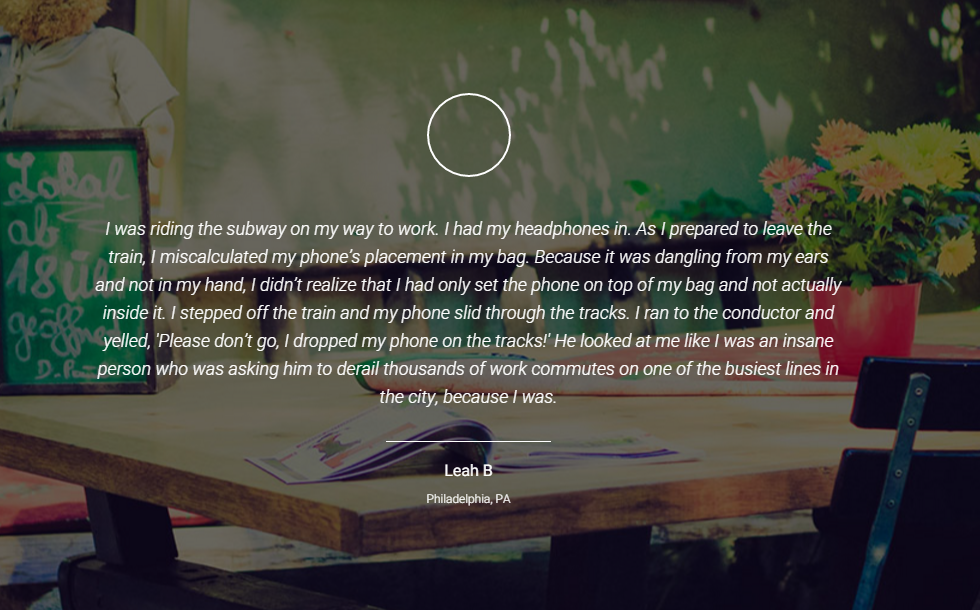

But to top it all off, the site seems to be lying on its face. The Penn page includes a quote from a “Leah B, Philadelphia, PA”:

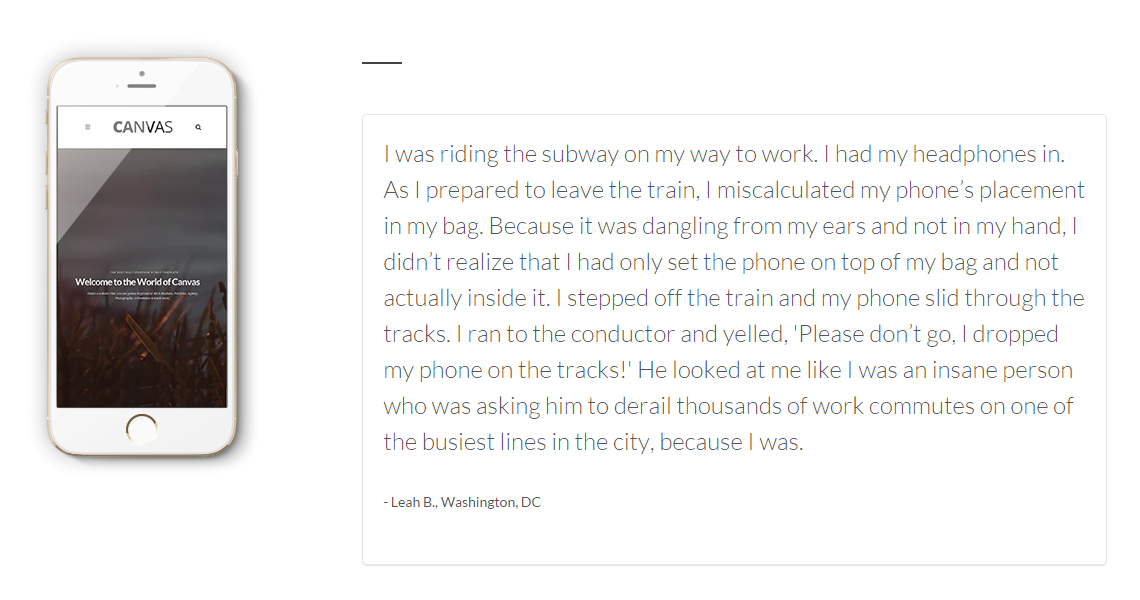

but the exact same quote is used on the non-Penn-branded homepage of GetCovered, this time from “Leah B, Washington, DC”!

As an alum, I certainly don’t want the university’s shield to be used in connection with this company. What they’re doing is strangely reminiscent of the Campus Backup service that OCM was marketing a few years ago — which shut down after my blog post overtook their site in search engines.

Previously, my site tagline was “News, technology, life, and more.”

As of today, it is now “Technology, law, life, and more.”

When I first started this blog in 2008, I labelled it “A blog discussing current events, news, politics, technology, law and more.” Even then, as a high schooler, I was interested in the law—and in the intersection of law and technology.

I distanced myself from law for a while, enticed by opportunities in engineering and medicine, right around the time I was applying to university and completing my first year of undergrad. Mirroring this stage of my life, I removed the keywords “politics” and “law”. I bloggedabouthealthcare-related issues.

As I now decide between two fantastic law schools to attend next year, I’ve realized that myentirepathhasbeenleadingme to this intersection of law & technology. But no matter where I go, I will always be a technologist first; the order of words in “Technology, law, life, and more” reflects that (and the deliberate Oxford comma).

It was time to update my blog to publicly acknowledge my choice of path in life—indeed, my return to my true passions.

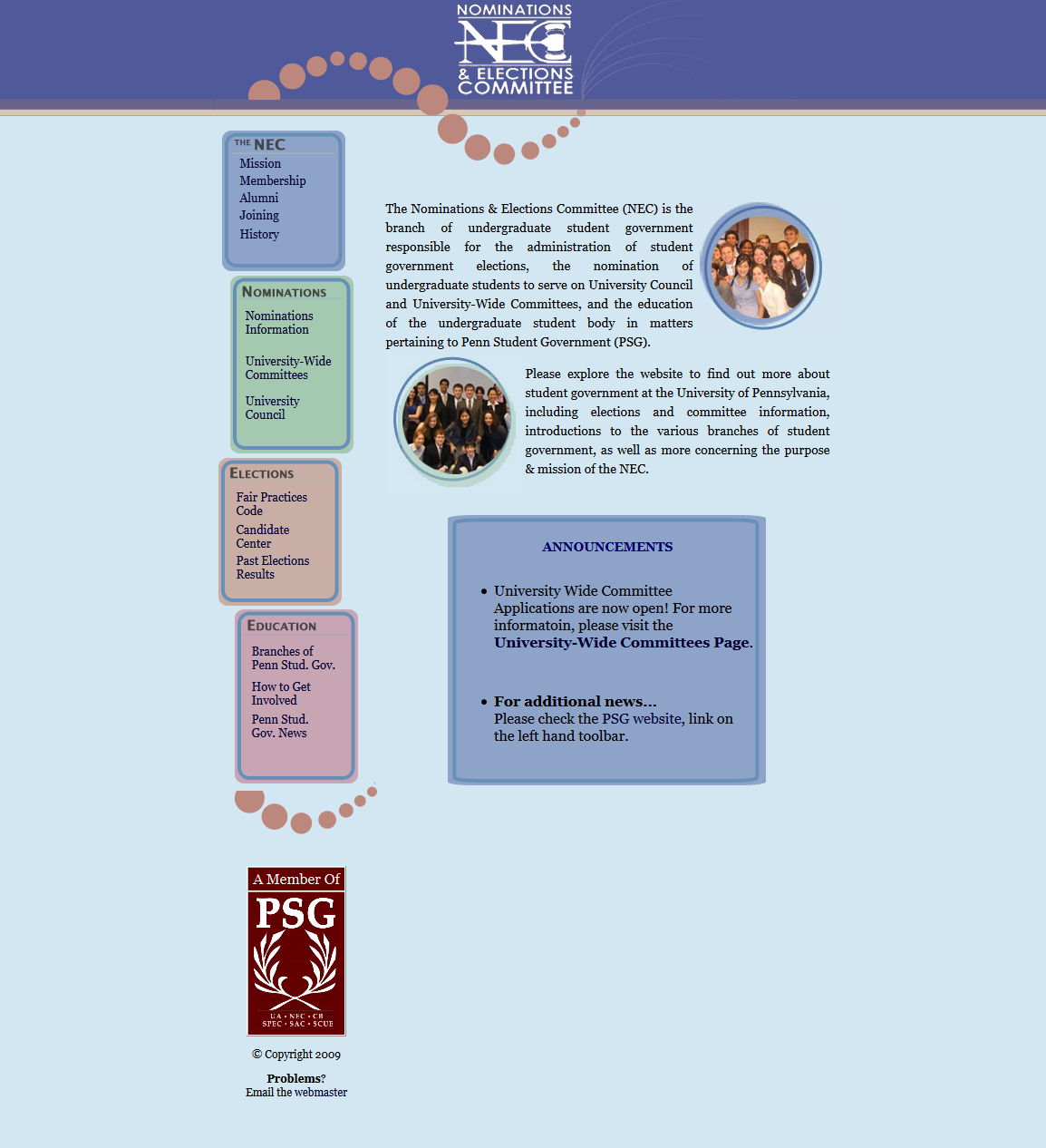

When I first came to Penn, the website for the Nominations & Elections Committee looked like this:

No, this wasn’t the year 1999… this was in 2011.

NEC website redesign

I set out to redevelop and redesign this, upgrading it from a static HTML site edited over SFTP to a WordPress CMS on Canvas. More importantly, the website redesign in 2012 needed to fit the rebranding that Penn underwent that academic year. In other words, I wanted it to look more like the university’s design. (An email to the Communications office responsible for web assets clarified that we could, in fact, do this.)

“Stable ownership is the gift of social law, and is given late in the progress of society. It would be curious then, if an idea, the fugitive fermentation of an individual brain, could, of natural right, be claimed in exclusive and stable property. If nature has made any one thing less susceptible than all others of exclusive property, it is the action of the thinking power called an idea, which an individual may exclusively possess as long as he keeps it to himself; but the moment it is divulged, it forces itself into the possession of every one, and the receiver cannot dispossess himself of it. Its peculiar character, too, is that no one possesses the less, because every other possesses the whole of it. He who receives an idea from me, receives instruction himself without lessening mine; as he who lights his taper at mine, receives light without darkening me. That ideas should freely spread from one to another over the globe, for the moral and mutual instruction of man, and improvement of his condition, seems to have been peculiarly and benevolently designed by nature, when she made them, like fire, expansible over all space, without lessening their density in any point, and like the air in which we breathe, move, and have our physical being, incapable of confinement or exclusive appropriation. Inventions then cannot, in nature, be a subject of property. Society may give an exclusive right to the profits arising from them, as an encouragement to men to pursue ideas which may produce utility, but this may or may not be done, according to the will and convenience of the society, without claim or complaint from anybody.”

VI Writings of Thomas Jefferson, at 180—181 (Washington ed.), as quoted in Graham v. John Deere Co., 383 U.S. 1 (1966). Emphasis mine.

I am not a tax attorney or tax consultant. This post was written while I was an undergraduate student at the University of Pennsylvania, and Co-Chair of the International Student Advisory Board.

Universities often will choose not to issue this tuition statement to international students because those students can’t do anything with it. This is, however, an incorrect generalization.

Are international students able to use this form for anything?

Most international students are ineligible to claim those educational credits/deductions because they are nonresident aliens (e.g. F-1 student). These individuals would not benefit from having the 1098-T.

But some students, especially graduate students, may be eligible to claim credits/deductions because…

they are resident aliens under the substantial presence test, usually because they have stayed in the United States for more than 5 years;

they are nonresident aliens for immigration purposes, but resident aliens for tax purposes, maybe as spouses of American citizens or resident aliens; or

they are nonresident aliens for both immigration and tax purposes, but eligible dependents of parents who are resident aliens/permanent residents/citizens; those parents are able to claim these credits in certain situations.

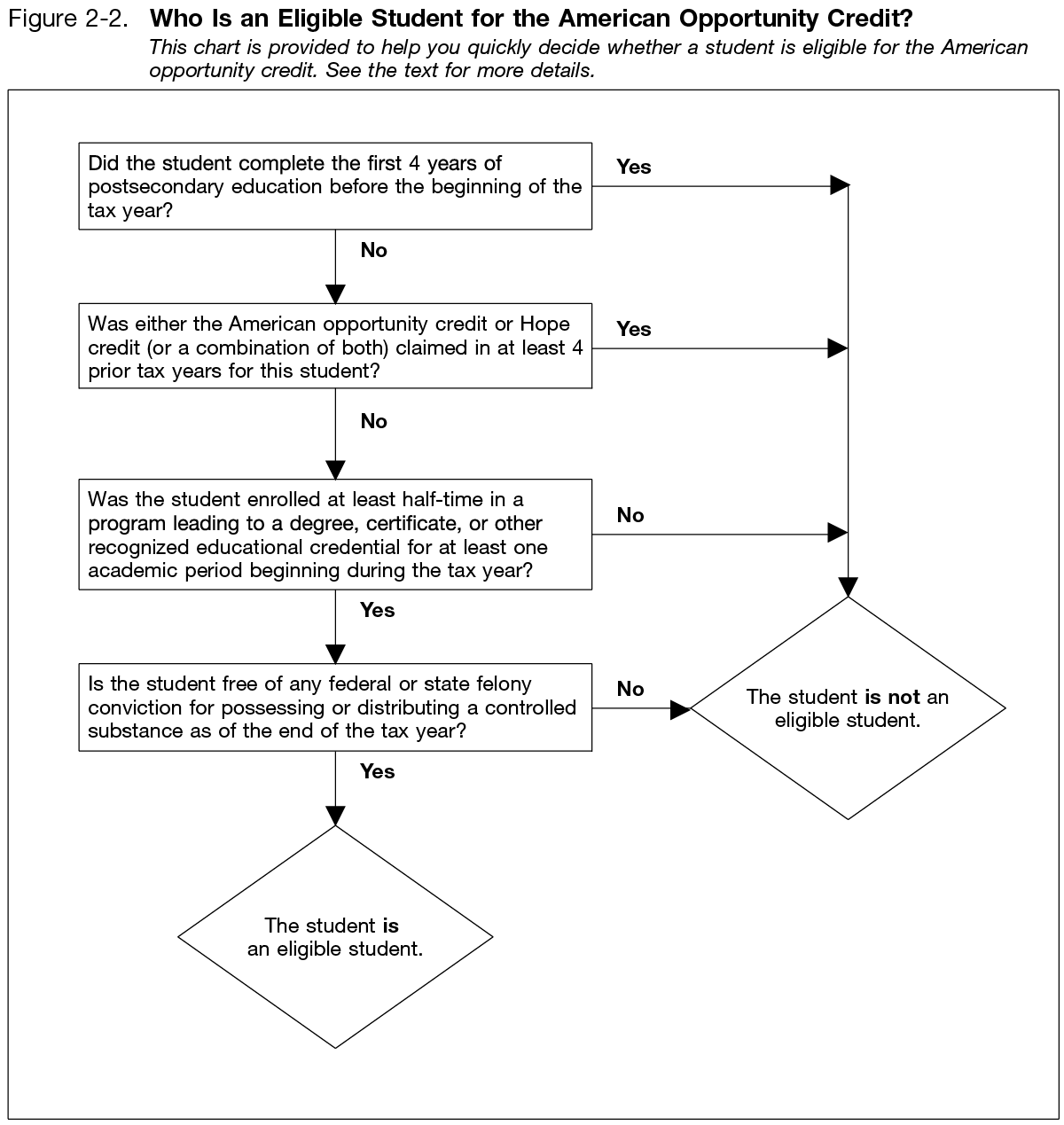

Figure 2-2 from IRS Publication 970, illustrating who is an eligible student for the American Opportunity Credit. Note: not all eligible students can claim. See Publication 970 for a flowchart of who is eligible to claim.

I am an international student in the above categories. Can I get a 1098-T from my school?

The IRS says that universities “do not have to file Form 1098-T or furnish a statement for… nonresident alien students, unless requested by the student“. Additionally, they are not required to provide it for “students whose qualified tuition and related expenses are entirely waived or paid entirely with scholarships”.

You must still meet all of the other requirements to get a 1098-T:

Attend an eligible educational institution (college, university, vocational school, or other postsecondary educational institution in §481 of the Higher Education Act)

Have paid qualified tuition and related expenses in that tax year

i.e. tuition, fees, course materials required to be enrolled

does not include room, board, insurance, medical expenses including student health fees, transportation, and personal/living/family expenses

Receive credit for the completion of course work leading to a postsecondary degree, certificate, or other recognized postsecondary educational credential

i.e. most undergraduate bachelors programs and graduate masters and PhDs qualify

Have provided your SSN or ITIN to the educational institution either through student records or an additional Form W-9S

What are some potential hurdles?

I was in a situation this year where my university did not issue me a 1098-T, and responded to my request with a form letter:

Does every Penn student receive a 1098-T? Penn does not provide a 1098-T to non-resident aliens, or any student whose qualified charges are fully funded by grant, scholarship or tuition waivers, or any student who was enrolled in non-credit courses during the academic year.

They additionally stated,

“Though you might have received a 1098t form in the past, going forward as a Canadian citizen you will not receive one.”

As I’ve explained above in this post, this determination was a mistake. It conflates citizenship & immigration status with residency for tax purposes, and ignores the possibility that someone else other than me may be eligible to claim the credit.

Furthermore, even if I were a nonresident alien ineligible to claim the credit, nothing in the IRS regulations for Form 1098-T gives the educational institution the right, responsibility, or power to determine whether I might be eligible to claim the credit; nor does it permit them to deny a Form 1098-T to a nonresident alien’s request.

What does this situation reveal about international students?

First, on the superficial level, this situation reveals that immigration status and residency for immigration purposes differs from tax status and residency for tax purposes. Clearly, not all employees who handle these cases are aware of these stipulations.

More importantly…

International students are a large, diverse, and varied community. International students have complex needs based on their individual families’ statuses. It is a mistake to define broad, indiscriminate policies that treat all international students identically.

If you think I’ve made a mistake in this post, or wish to disagree with my conclusion here, I’d like to hear from you. Comment below or send me an email using the contact form.

The Renaissance was marked by an explosion in the diffusion of ideas, and the naissance of the scientific method that has allowed us to explore this world. This was the time of Copernicus, Galileo, Michelangelo, and da Vinci — the last of which, far from being just a scientist and artist, was also an engineer and writer: the stunning definition of a Renaissance man.

And one of the founding fathers of the United States of America, Benjamin Franklin — also the founder of our alma mater — was a polymath himself. Politician, scientist, writer…

There is a reason we honour and respect figures like da Vinci and Franklin, even if we, enlightened with 21st century practicality, do not expect to educate the entire populace in their image.

We agree that there are serious deficits in the North American educational system that are in need of redress. We also concur that it is impractical to teach higher math effectively to every high school and college or university student. But we are firm in our belief that lowering the bar isn’t the answer. Andrew Hacker has a limited view of mathematics that fails to appreciate its value, and his solution of removing math from standards is flawed.