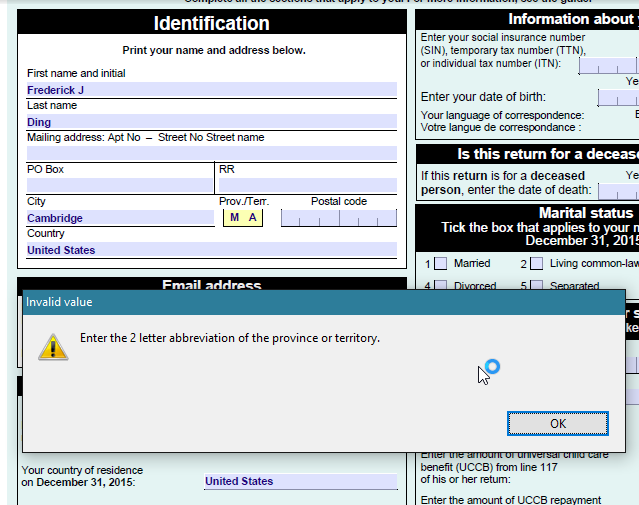

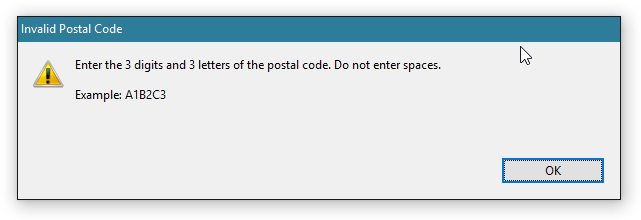

While trying to file my Canadian taxes as a nonresident, using the “Income Tax and Benefit Return for Non-residents … of Canada” — since I live in the United States and am a tax resident of the United States — I ran into a really frustrating bug in the first 5 form fields.

The form doesn’t accept non-Canadian provinces/territories and postal codes!

MA? not allowed.ZIP code? not allowed.

It’s really foolish, because many of the people who would be filing this form are likely residing outside of Canada. That’s why this version of the T1 return has an added Country field in the address block.

This is the kind of situation when PDF forms should just step back and allow free-form, unvalidated input.

There’s a provision that allows aliens in the U.S.[1] to choose to be treated as a U.S. resident for tax purposes even if they would not otherwise qualify as a resident. Income tax rules themselves are already really confusing — and they are even more complicated for foreigners in the U.S. — so a typographic error could really confuse a taxpayer.

I think the IRS made a typographic error, but I’m not even sure how to get in touch with them to fix this.

Motivating example

Suppose you arrive in the U.S. for the very first time on October 1, 2015 to work for the foreseeable future on a TN-1 (NAFTA Professional) visa. Because the period from 2015-10-01 to 2015-12-31 is insufficient to meet the Substantial Presence Test,[2] you would otherwise be a nonresident alien for tax year 2015. This would mean your income in the United States might be subject to taxation in the U.S. as well as in your home country. What if you wanted to be treated as a resident alien starting on October 1, 2015 — despite not satisfying the Substantial Presence Test?

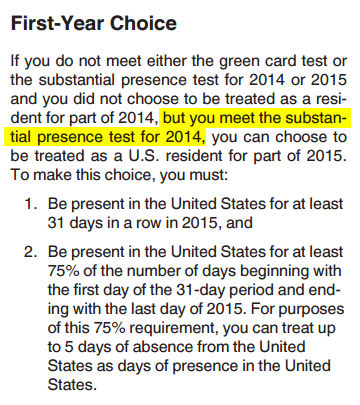

I got a little confused when I first read the rule, because it seemed to require an impossibility:

Let me excerpt that to show why it’s so self-contradictory: “If you do not meet either the [GCT] or the [SPT] for 2014 … but you meet the [SPT] for 2014.”

Huh? Clearly they meant 2016 there. Moreover, if you met the SPT for 2014, the current tax year — 2015 — wouldn’t be your first year in the U.S.

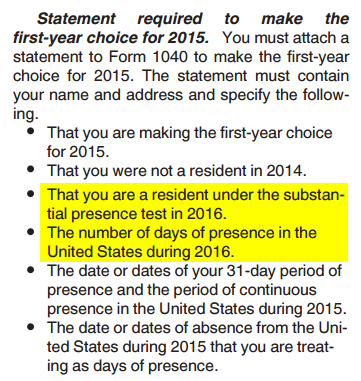

This is confirmed by the bulleted list on the following page:

Motivating example resolved

If you are going to satisfy the Substantial Presence Test in the following tax year — 2016 — you can choose to pretend to be a U.S. resident from 2015-10-01 to 2015-12-31 as well, if you meet all of the requirements in the bulleted list above.

The Substantial Presence Test (SPT) requires, in its simplest form, at least 183 days of physical presence within the United States in a three-year period.

I am not a tax attorney or tax consultant. This post was written while I was an undergraduate student at the University of Pennsylvania, and Co-Chair of the International Student Advisory Board.

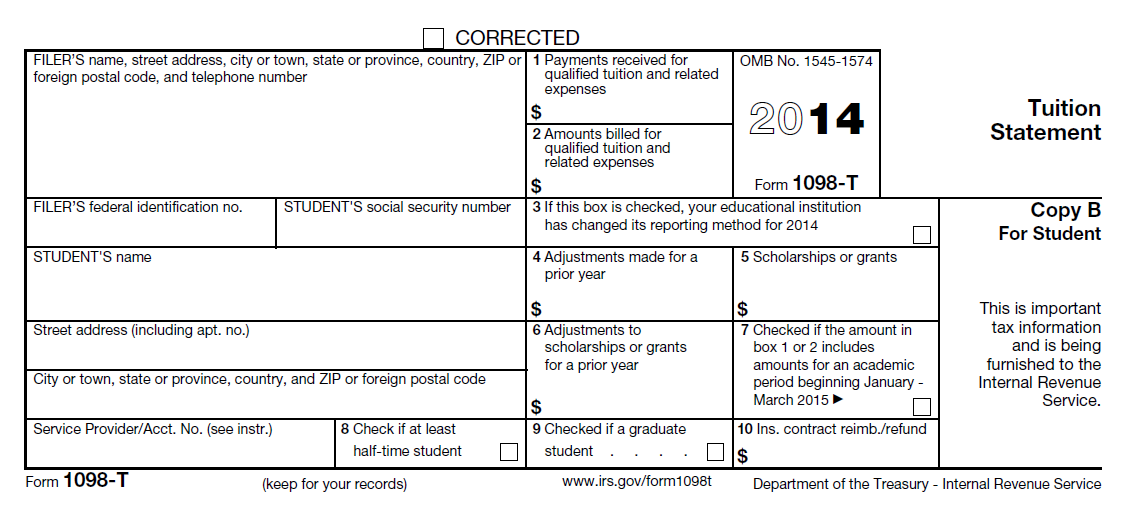

Universities often will choose not to issue this tuition statement to international students because those students can’t do anything with it. This is, however, an incorrect generalization.

Are international students able to use this form for anything?

Most international students are ineligible to claim those educational credits/deductions because they are nonresident aliens (e.g. F-1 student). These individuals would not benefit from having the 1098-T.

But some students, especially graduate students, may be eligible to claim credits/deductions because…

they are resident aliens under the substantial presence test, usually because they have stayed in the United States for more than 5 years;

they are nonresident aliens for immigration purposes, but resident aliens for tax purposes, maybe as spouses of American citizens or resident aliens; or

they are nonresident aliens for both immigration and tax purposes, but eligible dependents of parents who are resident aliens/permanent residents/citizens; those parents are able to claim these credits in certain situations.

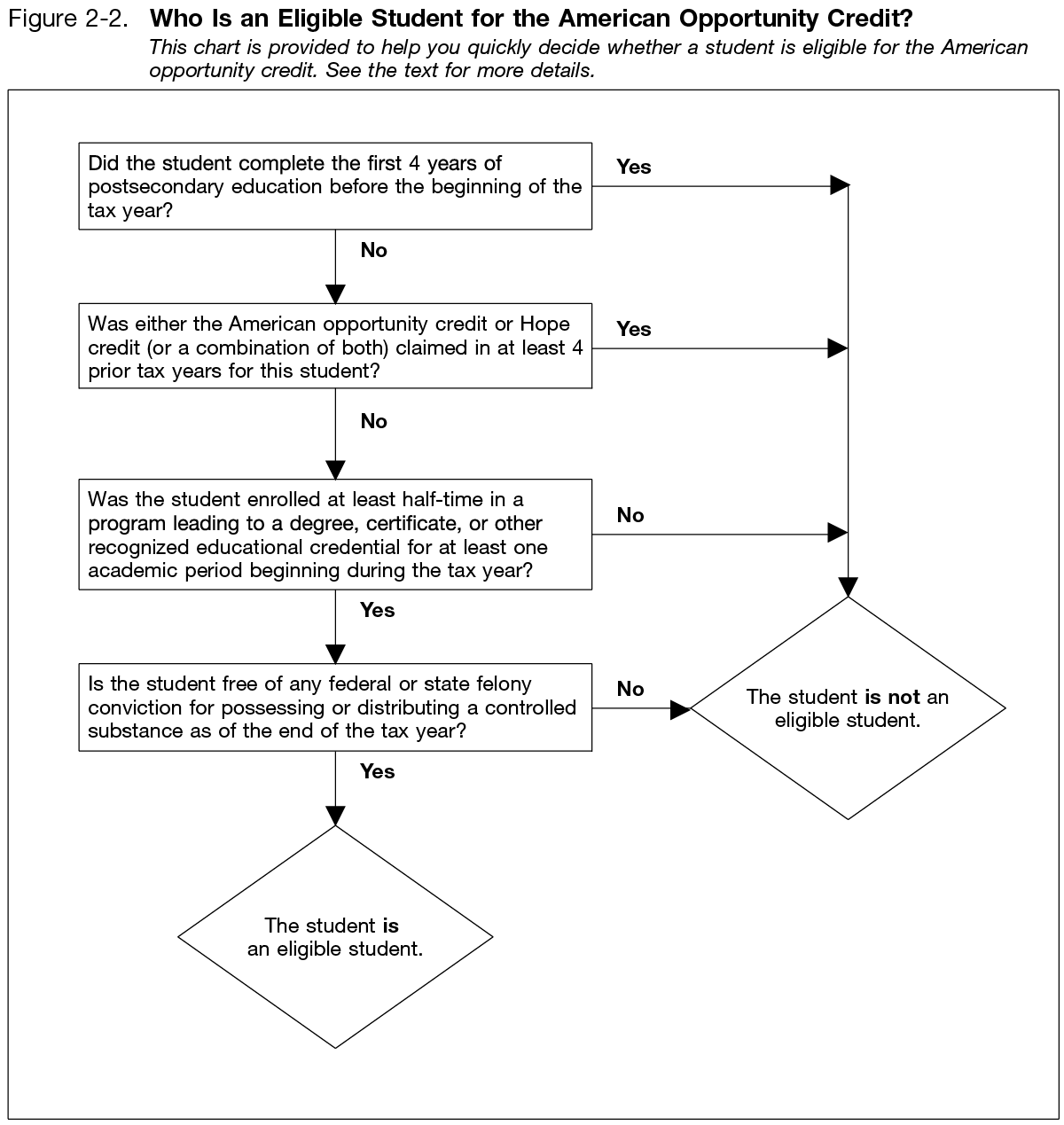

Figure 2-2 from IRS Publication 970, illustrating who is an eligible student for the American Opportunity Credit. Note: not all eligible students can claim. See Publication 970 for a flowchart of who is eligible to claim.

I am an international student in the above categories. Can I get a 1098-T from my school?

The IRS says that universities “do not have to file Form 1098-T or furnish a statement for… nonresident alien students, unless requested by the student“. Additionally, they are not required to provide it for “students whose qualified tuition and related expenses are entirely waived or paid entirely with scholarships”.

You must still meet all of the other requirements to get a 1098-T:

Attend an eligible educational institution (college, university, vocational school, or other postsecondary educational institution in §481 of the Higher Education Act)

Have paid qualified tuition and related expenses in that tax year

i.e. tuition, fees, course materials required to be enrolled

does not include room, board, insurance, medical expenses including student health fees, transportation, and personal/living/family expenses

Receive credit for the completion of course work leading to a postsecondary degree, certificate, or other recognized postsecondary educational credential

i.e. most undergraduate bachelors programs and graduate masters and PhDs qualify

Have provided your SSN or ITIN to the educational institution either through student records or an additional Form W-9S

What are some potential hurdles?

I was in a situation this year where my university did not issue me a 1098-T, and responded to my request with a form letter:

Does every Penn student receive a 1098-T? Penn does not provide a 1098-T to non-resident aliens, or any student whose qualified charges are fully funded by grant, scholarship or tuition waivers, or any student who was enrolled in non-credit courses during the academic year.

They additionally stated,

“Though you might have received a 1098t form in the past, going forward as a Canadian citizen you will not receive one.”

As I’ve explained above in this post, this determination was a mistake. It conflates citizenship & immigration status with residency for tax purposes, and ignores the possibility that someone else other than me may be eligible to claim the credit.

Furthermore, even if I were a nonresident alien ineligible to claim the credit, nothing in the IRS regulations for Form 1098-T gives the educational institution the right, responsibility, or power to determine whether I might be eligible to claim the credit; nor does it permit them to deny a Form 1098-T to a nonresident alien’s request.

What does this situation reveal about international students?

First, on the superficial level, this situation reveals that immigration status and residency for immigration purposes differs from tax status and residency for tax purposes. Clearly, not all employees who handle these cases are aware of these stipulations.

More importantly…

International students are a large, diverse, and varied community. International students have complex needs based on their individual families’ statuses. It is a mistake to define broad, indiscriminate policies that treat all international students identically.

If you think I’ve made a mistake in this post, or wish to disagree with my conclusion here, I’d like to hear from you. Comment below or send me an email using the contact form.